Have you ever wondered where unicorns come from? Mythology might have you thinking that unicorns have their origins in basements and garages, and while there are no shortages of these; unicorn startups share one thing in common – they are all conjured up in a sandbox environment.

We are not talking about horse like creature playing in sand castles, but something else that is desirable. Our focus is on software as a service (SaaS) and Independent Software Vendors (ISVs) that develop software applications. A sandbox account offers software developers a demo environment to code, build and test their application prior to going live in a production environment. Some of the best magic occurs here, like the development of unicorns.

With Software Innovation, Comes Competition; With Competition Comes Customer Demands

With 99% of businesses utilizing a minimum of one SaaS solution, there are endless amounts of new software companies popping up to streamline business operations for companies who do not have the resources to develop in-house solutions. From broad software solutions for membership management, campaign management, club management and ERP software; to focused software solutions for retail, lodging, wholesale, florists and even nail salon or grocery point of sales; there are software applications available for every vertical and market. This is a sign of innovation and progress, we can perform any task imaginable from placing an order, to sending an invoice to self-checkout; but it also means higher expectations and demands from the end user and companies using the software applications. A segmented growing list of applications is a concept of the past. Today, independent software vendors and their developers are galloping to keep up with constant feature releases, updates, and added modules for their users; to offer one software application that can be customized on the fly. So, for ISVs where downstream users are businesses, and many of their tasks include monetary transactions with their own customers, what do software providers do when their users are looking to add payment capabilities?

Pairing Software Solutions with Payment Technology

When businesses are looking to add payment functionality to their operations, it can be anything from one click payments to complex payment systems. Software companies used to redirect their users to 3rd parties for these functions, and to stay competitive some tried to offer in-house payments. Along they way they spread themselves too thin by losing focus on their software expertise. Today they can easily leverage the payment processing infrastructure and payment API (application programming interface) connections to offer customized omni commerce integrated payment processing solutions. When an ISV adds payment partners with industry expertise to their ecosystem, they can offer embedded payments. The result: payment processing converges with business management for a centralized application, and with built-in payments, there is no longer a need to redirect; payments are accepted within the software.

Optimize Your Software Payment Offerings with Cartis

You may already offer integrated payments; or you may be looking to integrate payment processing for the first time. That means you already know the intrinsic value it has to customer experience and the demands of reducing manual labour, errors, and costs. While we can extensively cover the benefits of integrated payments, it is more important to bring to light strategic insights and options to make sure you are checking off all the right boxes for providing a seamless checkout experience for your users and their customers. Optimizing your software features sometimes means turning to someone else’s expertise to learn about the offerings you didn’t even realize your users need. Adding Cartis to your payments ecosystem also means letting us check off all the boxes for what you are looking to accomplish with your integration project.

One key element to optimizing your payment offering is the reduction of payment friction. Software developers and those with limited payment expertise tend to get stuck and go with a quick solution. Whether this be choosing to integrate to Stripe, integrating to open payment gateways like Authorize.Net, Bambora / Worldline or CyberSource, or even integrating to all of them. While the idea of multiple providers, open gateways and quick solutions seem attractive, they create barriers that have a hindrance on merchant processing for your users, and by extension to the payment relationship for your software application. Other than losing control of your user relationship and losing time in maintaining multiple integrations and payment vendor partnerships; when a problem arises, these systems offer little support and a great deal of friction. Effectively, you are redirecting your users to solutions outside of your payment infrastructure. Many of these gateways have too many connections they themselves are trying to maintain, and with their limited bandwidth it is easy for them to become out of date in their certification to acquirers. This can create issues for merchant processing, like higher declines due to limited data being passed through to the acquiring banks and card issuers. More importantly, they lack functionality to offer evolving businesses and your users. For instance, if your user wants to accept multiple currencies, they will need separate gateway IDs through these providers.

While these options all help your users accept ecommerce payments, they tend to be limited in functions and value beyond that. A business does not operate within a vacuum, as they evolve to their environment and their customers, they need pricing flexibility, and global omnichannel payment functionality that will evolve with them.

Two-Pronged Payments Approach

We understand that when choosing an ecommerce payment system, software companies may still have a need to go with the above route of open gateways for their users. That is why as an Elavon payments partner, Cartis has an approach in place to allow software companies and their users to maintain their gateway relationship, resulting in no software changes, but without sacrificing on their credit card processing options. If you have not integrated Elavon’s own payment gateway, Converge, with your software application, we are still able to connect your software through the pre-established relationships (value added resellers), and direct to host integrations of these open gateways to Elavon for processing. This allows Cartis Payments to work with you and your users, regardless of payment gateway.

The second approach is making payment integrations seamless and simple. Whether you are a merchant or a software developer looking to integrate payments into your SaaS, into an existing ecommerce solution, accept payments online, through webforms, in person or through a mobile app; between Elavon’s Tetra Semi-Integrated Solution and Elavon’s Converge omni commerce payment gateway you can code to any payment environment through robust payment APIs (application programming interface) and SDKs (software development kit). Better yet, use one simple API for card present and card not present payment acceptance across North America.

Addressing Payment Integration and Payment Partnership Questions

From the starting gate, with a dedicated solution engineer, we review the payment solutions you are looking for and what you are trying to accomplish in the scope of your payment integration project. We will review the obstacles and issues you may be facing with your current credit card processing integration and how those can be addressed, and will work with you through integration development, certification, future user acceptance testing (UAT), merchant onboarding and maintaining the relationship.

We have the support, service, and expertise, but can we outperform?

For your evaluation, instead of providing you with the questions you should ask, we are providing real obstacles discussed by SaaS providers and the questions that have been asked by ISV partners and prospects so you can evaluate how the answers and issues are addressed against our competitors and your requirements.

Q: What developer tools are available?

A: We ensure you have the resources needed for your testing environment. This includes a dedicated solution engineer for ongoing support, developer portal, sample code, a demo / sandbox account with API credentials and demo devices where applicable.

Q: With our current integration they do not offer our clients credit card terminals or credit card readers for card present rates. Do you have these offerings?

A: Many gateway integrations do not have card present offerings. We offer a line of Ingenico smart credit card terminals, EMV PIN pads, and EMV credit card readers that can be used as standalone terminals for your clients and/or that can be integrated to your software.

Q: What custom payment integrations do you support?

A: For integrating payments through a website (ecommerce) and integrating payments in a mobile app you would be looking at a Converge payment gateway integration and are able to utilize a hosted payments integration: hosted payment page (HPP), Lightbox, Checkout.js or XML API.

For integrating a desktop or mobile point of sale (MPOS) like a cash register using a tablet for card present payments you would be looking at our Commerce SDK (CSDK) integration if you require tokenization or for in person payments on a terminal (card present) that does not require tokenization

you can make your point-of-sale EMV compliant through terminal semi integration.

For an open gateway integration specific to the travel and entertainment (T & E) industry or property management systems (PMS) integrations we offer the Fusebox gateway integration.

Q: What integrations are available for existing shopping cart and ecommerce platforms that our clients are using?

A: We offer a simple method of integrating exiting shopping carts or content management systems (CMS) like WooCommerce, Magento, and BigCommerce with the Converge payment gateway through pre-established relationships as well as using Elavon’s free in-house shopping cart plugins.

Q: What mobile wallet support do you offer?

A: Certain Converge integrations allow you to integrate with Google Pay and Apple Pay to process payments on the web.

Q: How do we ensure our software application is within Payment Card Industry PCI guidelines?

A: We review with you the methods that allow your software application to have access to primary account number PAN data which would require you to complete annual complex PCI audits as well as those payment solutions that allow you to remain outside the PCI scope and to offload PCI scope to Elavon.

Q: Are you able to serve both Canadian and US merchants?

A: Yes, we can serve both Canadian Merchants and US merchants.

Q: What card brands do you support?

A: We support all card types: Visa, Mastercard, American Express, Discover / Diners, Japan Credit Union (JCB), China UnionPay (CUP), Interac (Canada card present), and more…

Q: With our current integration, for our clients to sign up to accept Amex is a complicated process, with multiple forms and applications and no support for USD transactions. How do you handle onboarding Amex acceptance?

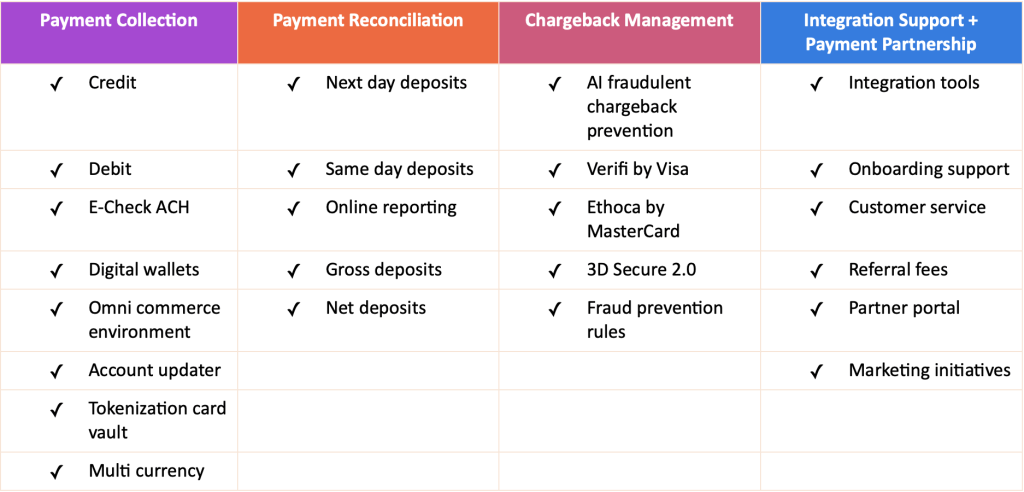

A: We handle direct boarding and support of American Express up to $1M annually through their OptBlue program with no additional paperwork for both CAD and USD transactions. Amex deposits are funded on a daily basis as part of the daily settled batch.

Q: Our clients currently experience a 3-day funding credit lag. Do you offer quicker funding times?

A: Batches that are settled by 10PM EST are funded the same day with deposits received the following morning. US merchants have the option to add next day funding, fast track funding and true daily funding for same day deposit options, as well as instant funding for real-time deposits within minutes.

Q: Clients with our current provider find reconciling bank accounts with the accounting system is a mess because of a net fee structure the fees are taken out of the amount charged.

A: We offer both funding options: daily discount (net) and gross deposit. Our default to is to gross deposit where the client will receive 100% of amount charged daily. A statement is produced each month and owed fees will automatically be withdrawn on the 1st of the following month.

Q: Do clients have access to any reporting tools for reconciliation outside of our software reporting?

A: Each client receives access to a complimentary reporting tool to view online statements and generate reports of daily settlements and deposits.

Q: Do you do a fixed rate, interchange plus or either option depending on our preference?

A: We offer both pricing structures and work with you to set up a competitive pricing program structure that is both beneficial to you and your downstream clients.

Q: What would merchant application process look like for our clients?

A: Merchants would complete our online application request form and we would put together their application which are signed electronically. Applications are either approved by an instant decision engine or within 24 hours. We can also prepare a co-branded custom form that you can embed on your website.

Q: Are you able to board our clients that want to continue to use their current gateways (Bambora, NMI, CyberSource, Authorize.Net, Pay Flow Pro, USAePay…) but get the above benefits?

A: Yes, your clients would continue to utilize your integration to those gateways with a gateway only account and the processing would be handled through us. Most open gateways have a direct integration to Elavon (the processor we work with). We would send the merchant a VAR sheet with the terminal ID to be plugged in to their gateway to program the processing to us.

Q: How many merchant accounts does a client need to support their card present, card not present and ecommerce transactions?

A: With our single MID solution, your clients only need one application, one sign up, and one account that will handle all processing environments.

Q: Clients using our current gateway provider need a separate gateway ID for each currency, is it the same with you?

A: We offer multi-currency conversion through one gateway account allowing your clients to sell online in 100 different currencies and receive the funding in their own currency.

Q: Some of our ecommerce clients have a problem with fraudulent chargebacks, do you offer any fraud prevention or chargeback management?

A: We have a basket of add-on tools available for chargebacks prevention , to combat fraudulent chargebacks, and if using the Converge gateway there are integrated fraud prevention rules and technology that can be set up.

Q: Are you able to do a revenue share? What would a partner agreement look like?

A: Yes, whether you integrate with us or not, we will provide an attractive revenue share for onboarded merchants. Referral fees are calculated as a percentage of net income paid to Cartis arising out of your boarded merchants.

Q: Do you offer a partner portal?

A: Yes, you would be given login to our partner portal which will provide you with source data populated daily and partner referral residuals.

From completing an integration to onboarding and navigating payments, Cartis Payments provides quality support and unparalleled advisory service to our software partners and their clients. We have the payment technology, the payment infrastructure and the payment experience that you will want to add to your software payments ecosystem. We play a role in each others success, so come play in our sandbox!